TradeVisor Broker Review

This article provides a comprehensive analytical review of TradeVisor (tradevisor.ai), a platform that presents itself as a copy trading and automated trading service. Based on an examination of the official website, technical domain data, independent reviews, and user complaints, TradeVisor demonstrates multiple characteristics commonly associated with fraudulent or highly unreliable investment schemes. This review is written as an investigative exposure and should be read as a risk warning for potential investors.

Overview of TradeVisor

TradeVisor positions itself as a copy trading and automated trading platform focused primarily on the forex market, with claimed access to CFDs, cryptocurrencies, commodities, and stock indices. The website markets the service as suitable for beginners and emphasizes risk management, diversification, and professional strategies. It also claims that the service has been operating for more than ten years.

However, none of these claims are supported by verifiable evidence. The platform does not provide documented company history, audited performance records, or any public proof of long-term operation. Technical analysis of the domain and the absence of corporate disclosures directly contradict the claim of a decade-long presence in the market.

Legal Status and Regulation

One of the most serious issues with TradeVisor is the complete lack of regulatory transparency.

Key findings:

- No jurisdiction is disclosed on the official website.

- No licensed legal entity is named as the operator of the platform.

- No regulatory authority is mentioned.

- No license numbers or registration documents are provided.

TradeVisor is not listed in the registers of any major financial regulators, including but not limited to FCA, CySEC, ASIC, or other recognized supervisory authorities. This means the platform operates outside any recognized regulatory framework.

For financial services involving trading, copy trading, or management of client funds, regulation is not optional. The absence of licensing implies that clients have no legal protection, no access to compensation schemes, and no regulatory body to contact in case of disputes or losses.

Corporate Transparency and Ownership

TradeVisor does not disclose:

- The legal name of the operating company

- The country of incorporation

- Company registration numbers

- Names of directors, executives, or beneficial owners

- Physical office address

This level of anonymity is unacceptable for a financial service provider. Legitimate brokers and trading platforms are required to clearly disclose their corporate structure and legal responsibility. Anonymous operation is a common trait of scam platforms designed to disappear once sufficient funds are collected.

Domain and Technical Analysis

Technical checks of the tradevisor.ai domain reveal further red flags.

- The domain was registered recently, despite claims of over ten years of operation.

- There is no long-term digital footprint or historical web presence.

- Trust and security assessment services assign the domain an extremely low trust score.

- The website uses basic SSL encryption, which only secures data transmission and does not indicate legitimacy or regulatory compliance.

A newly registered domain combined with aggressive financial marketing is a well-known pattern among short-lived scam projects.

Trading Conditions and Platform Details

TradeVisor provides almost no concrete information about trading conditions.

Missing or undisclosed information includes:

- Account types

- Minimum deposit requirements

- Leverage limits

- Spreads and commissions

- Execution model (STP, ECN, dealing desk)

- Liquidity providers

- Order execution policies

The website claims support for MetaTrader 4 and MetaTrader 5, as well as automated trading tools, but does not explain how users connect to these platforms or which broker executes the trades. This raises serious questions about whether real market trading occurs at all.

Without transparent trading conditions, clients cannot evaluate costs, risks, or the realism of advertised returns.

Financial Instruments

According to the website, TradeVisor claims to offer trading access to:

- Forex currency pairs

- CFD instruments

- Cryptocurrencies

- Commodities

- Stock indices

However, there is no contract specification, asset list, or trading documentation confirming the availability or execution of these instruments. The claims remain purely promotional.

Deposit and Withdrawal Practices

TradeVisor does not clearly disclose funding or withdrawal procedures on its website.

Based on user complaints and reviews, the following issues have been reported:

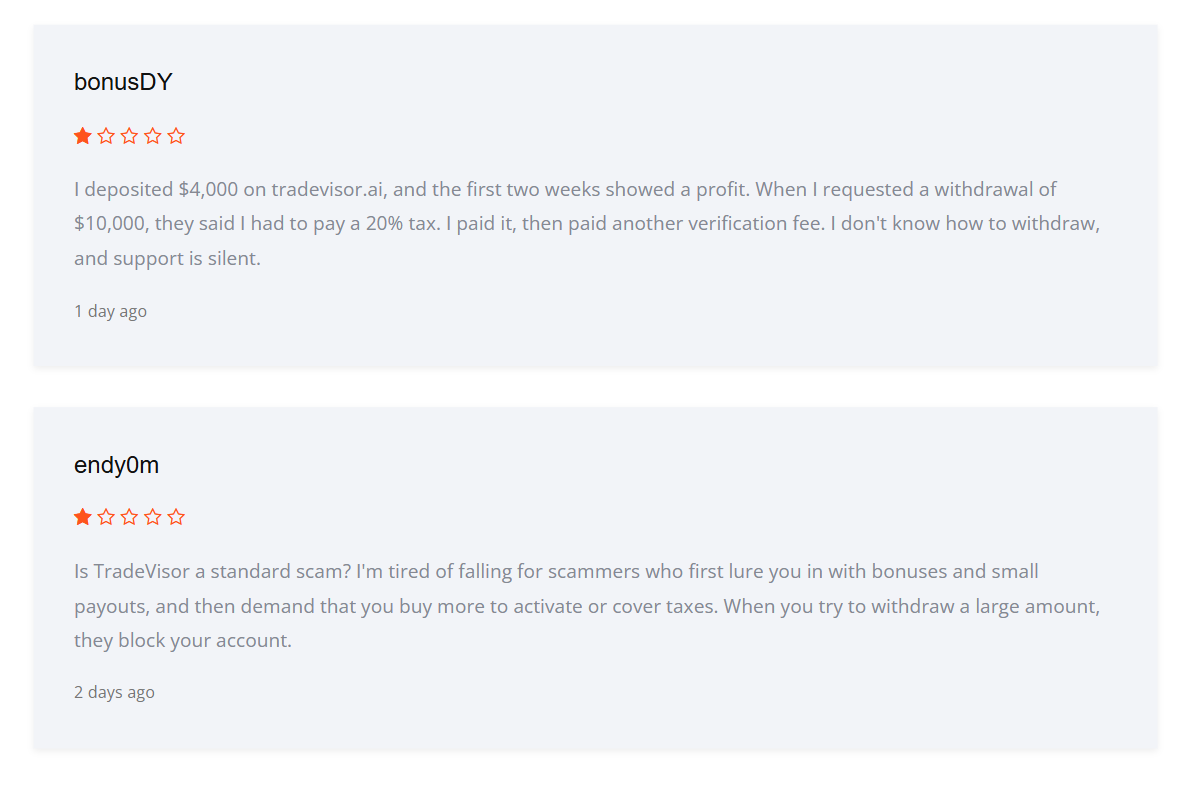

- Initial deposits are accepted without difficulty.

- Small profits may be shown on the platform interface.

- Withdrawal requests trigger additional demands, such as so-called taxes, verification fees, or activation charges.

- After payments are made, withdrawals are delayed or completely blocked.

- Customer support becomes unresponsive.

Requiring users to pay taxes or fees directly to the platform before withdrawals is not a legitimate brokerage practice. Taxes are paid to government authorities, not to private trading platforms. This is a common tactic used in fraudulent schemes to extract additional funds.

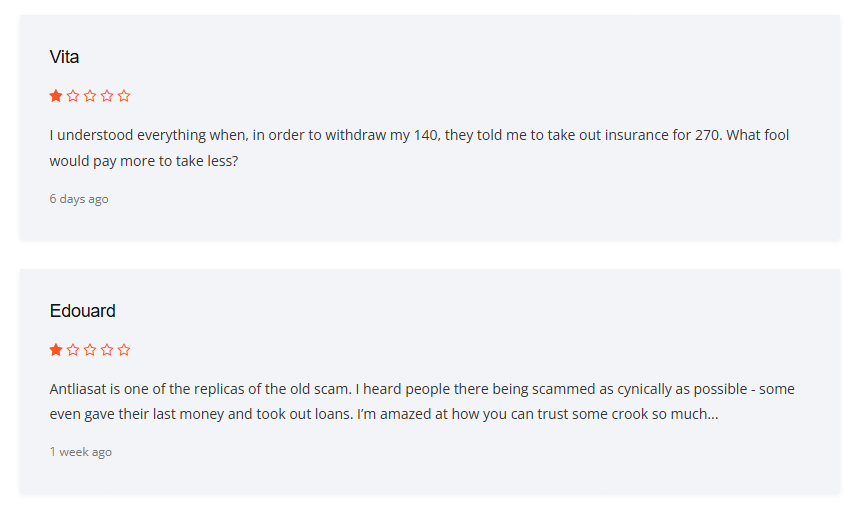

User Complaints and Reviews

Independent user feedback raises serious concerns.

Reported complaints include:

- Account blocking after profitable periods

- Sudden introduction of unexpected fees

- Inability to withdraw funds

- Lack of response from customer support

Some online platforms show positive reviews, but these are inconsistent with detailed complaints found elsewhere. Short, generic positive feedback without transaction details is often indicative of fabricated or incentivized reviews.

When negative reviews consistently describe the same withdrawal-related problems, they should be treated as credible warning signals.

Marketing Claims

TradeVisor relies heavily on marketing language rather than factual disclosures.

Problematic claims include:

- Statements about long-term operation without evidence

- Vague references to professional traders and advanced strategies

- Promotional educational content used to build trust rather than provide verified value

There is no independently verified performance data, no audited statistics, and no transparent methodology behind the advertised strategies.

Risk Assessment

Based on the collected information, TradeVisor presents the following high-risk factors:

- No regulation or licensing

- Anonymous ownership

- Recently registered domain

- Lack of transparent trading conditions

- Repeated complaints about withdrawal issues

- Use of non-standard and misleading fee demands

These factors align closely with known patterns of online investment fraud.

Conclusion

TradeVisor (tradevisor.ai) should not be considered a legitimate broker or a safe trading platform. The absence of regulation, corporate transparency, and verifiable trading infrastructure, combined with user complaints about blocked withdrawals and fabricated fees, strongly suggests that this platform operates outside legal and ethical financial standards.

Investors are strongly advised to avoid depositing funds with TradeVisor. Any platform offering trading or copy trading services without clear licensing, documented ownership, and transparent conditions poses a serious financial risk. In this case, the evidence points not to poor service quality, but to a structure that closely resembles a classic investment scam.

Comments

Tag Markets Broker Review

Kogza (kogza.com) Review

SSE-Trade (sse-trade.com) Broker Review

Lumoral Market Room Broker Review

DigBit Exchange Review