FSCS Review

The Financial Services Compensation Scheme (FSCS) is the UK’s statutory compensation scheme for customers of authorized financial services firms. It was established to provide financial protection when regulated firms fail and are unable to return customers’ money or meet their financial obligations.

Unlike investment insurance or portfolio protection, FSCS does not shield consumers from market losses. Instead, it serves as a financial safety net when an authorized bank, broker, insurer, or other regulated financial institution becomes insolvent.

Today, FSCS plays a vital role in maintaining confidence in the UK’s financial system and protecting millions of consumers.

Why FSCS Exists

Financial institutions are heavily regulated, but regulation alone cannot eliminate the possibility of business failure.

Banks can become insolvent, investment firms may cease trading, and insurance providers can experience financial distress. Without a compensation framework, customers could face significant financial losses even when using regulated providers.

FSCS was created to address this issue by providing compensation to eligible customers when authorized firms are unable to meet their obligations.

Its purpose is not to prevent financial failures but to reduce their impact on consumers and strengthen trust in the UK’s financial services industry.

What Financial Products Are Covered?

FSCS protects a broad range of financial products offered by authorized firms.

Coverage may include:

- Bank accounts

- Savings accounts

- Cash ISAs

- Investment services

- Insurance policies

- Pension advice

- Mortgage advice

- Debt management services

- Certain payment-related services

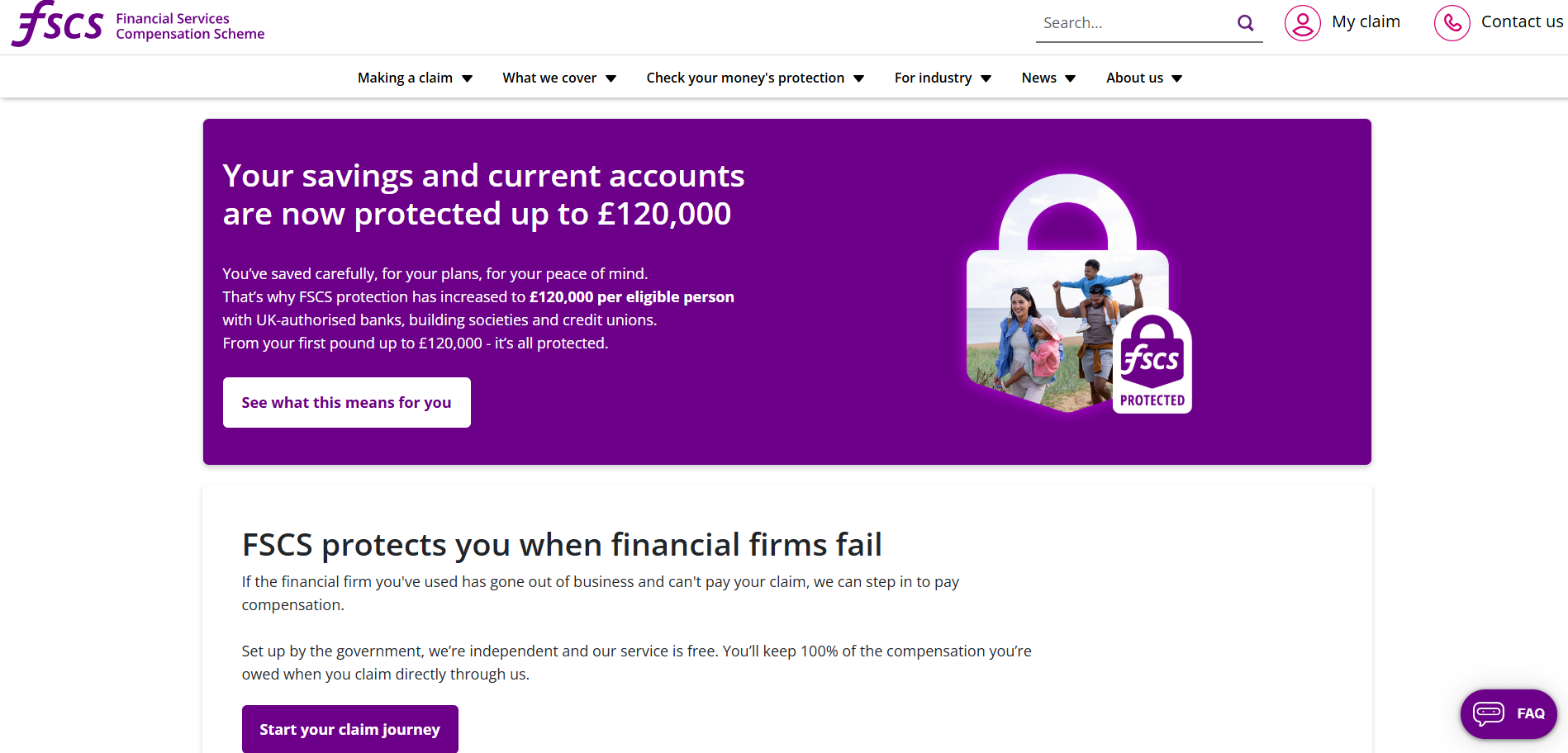

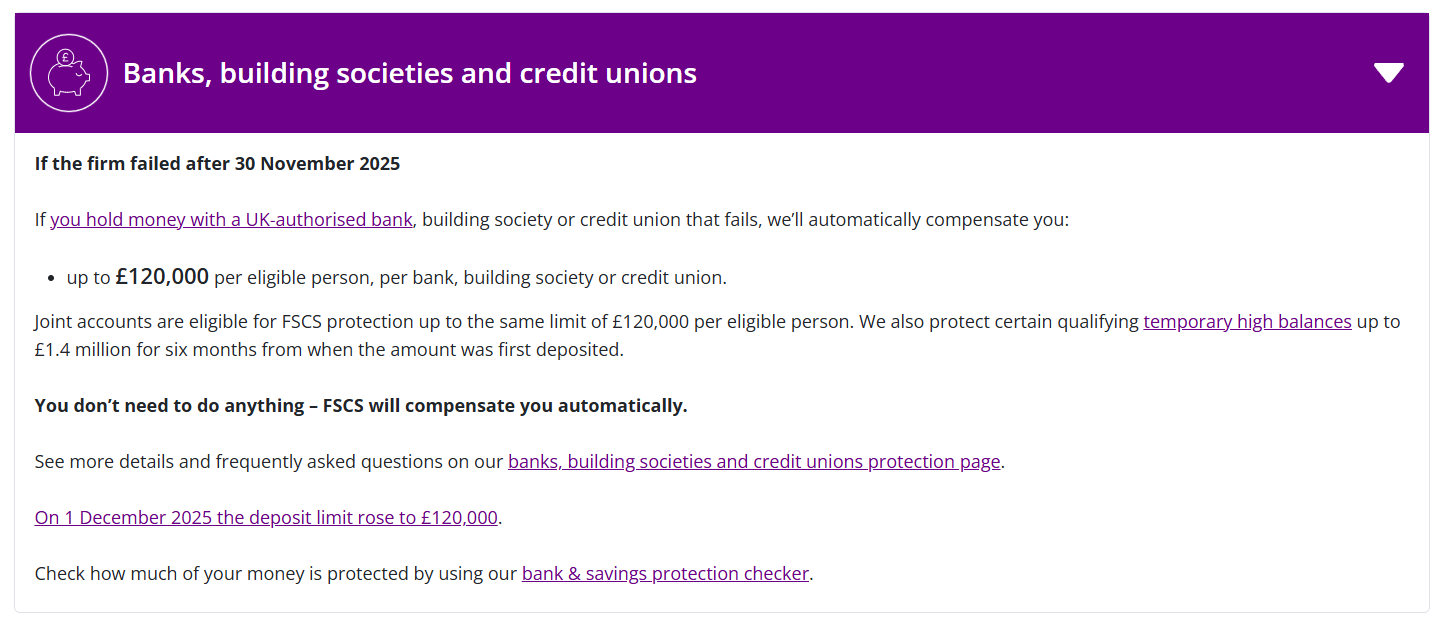

The level of compensation depends on the type of financial product involved and the applicable protection limits established under UK regulations.

Consumers should always verify that a financial institution is authorized before assuming FSCS protection applies.

When Compensation Applies

FSCS only becomes involved after a regulated financial firm has officially failed.

A typical compensation process includes the following stages:

- A financial services firm becomes insolvent or is declared in default.

- UK regulators determine that the firm cannot meet its obligations.

- FSCS reviews customer eligibility.

- Compensation is paid to eligible customers within the applicable limits.

For many deposit-related claims, customers receive compensation automatically without submitting an application.

More complex investment or insurance claims may require additional documentation and review.

Common Misconceptions

FSCS is often misunderstood, particularly by new investors.

One of the most common misconceptions is that FSCS protects against investment losses.

It does not.

FSCS does not compensate customers for:

- Declining stock prices

- Investment losses

- Cryptocurrency market volatility

- Poor trading decisions

- Unsuccessful investment strategies

- Losses caused by market conditions

Its protection only applies when a regulated financial firm fails and cannot return customer assets or fulfill its contractual obligations.

Understanding this distinction is essential when evaluating financial risk.

Is FSCS Enough Protection?

FSCS provides an important layer of financial security, but it should not be the only factor considered when choosing a financial institution.

Consumers should also evaluate:

- Regulatory status

- Financial stability

- Company reputation

- Risk management practices

- Customer service

- Transparency of products and fees

A regulated firm with FSCS protection offers additional peace of mind, but it does not eliminate investment or market risk.

Responsible financial decisions still require careful research and appropriate diversification.

Final Verdict

FSCS is one of the most important consumer protection mechanisms within the UK’s financial system. By compensating eligible customers when authorized firms become insolvent, it helps maintain confidence in banks, investment firms, insurers, and other regulated financial institutions.

Although FSCS does not insure investments or protect against market fluctuations, it provides valuable protection against one of the most significant operational risks facing consumers—the failure of a regulated financial services provider.

For anyone using UK-based financial institutions, understanding how FSCS works is an essential part of managing financial risk and making informed investment decisions.