Lloyd’s of London Review

Lloyd’s of London is one of the oldest and most respected names in the global insurance industry. However, despite its reputation, many people mistakenly believe Lloyd’s is an insurance company. In reality, it operates as a specialized insurance marketplace where multiple independent insurers, known as syndicates, provide coverage for complex and high-value risks.

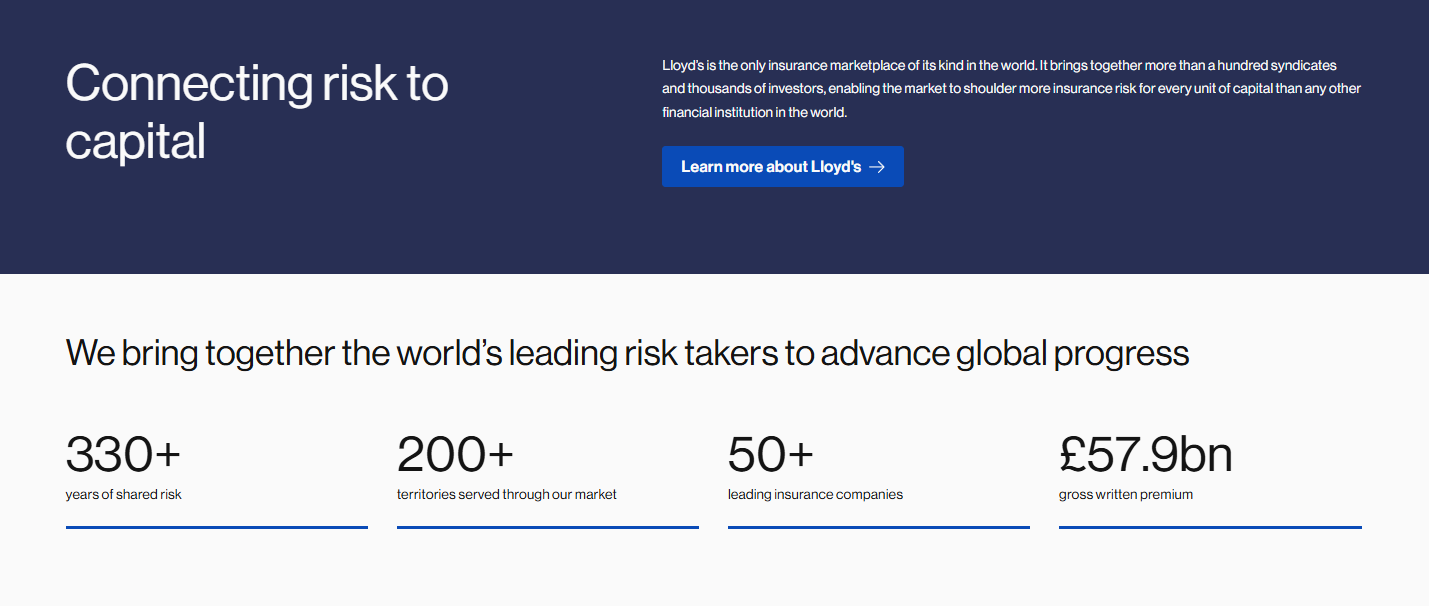

Founded in 1688, Lloyd’s has evolved into a global marketplace serving businesses in more than 200 countries and territories. Today, it plays a significant role in protecting financial institutions, multinational corporations, shipping companies, airlines, technology firms, and many other organizations that require specialized insurance solutions.

Rather than offering standard consumer insurance products, Lloyd’s focuses on risks that are often too large, too unusual, or too complex for a single insurer to accept.

Why Lloyd’s Is Different From Traditional Insurance Companies

One of the biggest misconceptions about Lloyd’s is that it functions like a conventional insurance provider.

Traditional insurers underwrite policies using their own capital and assume full responsibility for the insured risk. Lloyd’s follows an entirely different model.

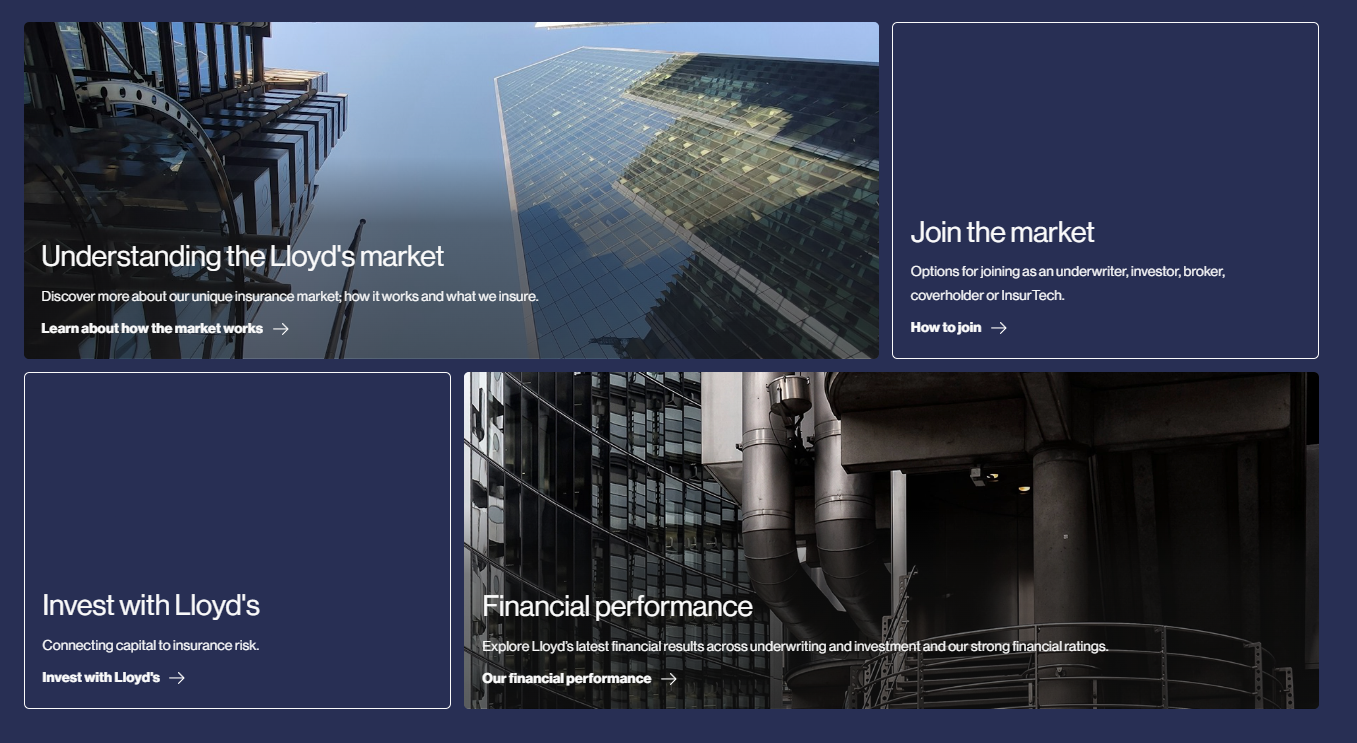

Instead of operating as a single insurer, Lloyd’s provides the marketplace where independent syndicates compete and cooperate to insure commercial risks. Each syndicate employs its own underwriting specialists, determines its own pricing strategy, and decides which risks it is willing to insure.

Because several syndicates can participate in the same insurance policy, very large risks can be divided among multiple insurers instead of relying on a single company.

This distributed model has become one of the defining characteristics of Lloyd’s and is one of the main reasons it remains a leader in specialty insurance.

How the Lloyd’s Market Operates

Insurance policies at Lloyd’s are typically arranged through licensed insurance brokers with direct access to the marketplace.

A simplified process looks like this:

- A business identifies a risk requiring insurance.

- A broker prepares detailed underwriting information.

- The submission is presented to one or more Lloyd’s syndicates.

- Each syndicate evaluates the opportunity independently.

- Multiple syndicates may agree to insure portions of the same policy.

- Together they create one comprehensive insurance contract.

This approach allows businesses to obtain insurance coverage that would often be unavailable through conventional insurers.

It also enables insurers to diversify their own exposure by sharing responsibility with other market participants.

What Types of Risks Are Covered?

Lloyd’s specializes in commercial and specialty insurance rather than personal insurance products.

Common areas of coverage include:

- Cyber insurance

- Professional indemnity

- Directors & Officers (D&O) liability

- Financial institution insurance

- Marine and cargo insurance

- Aviation insurance

- Political risk

- Energy projects

- Construction risks

- Space and satellite insurance

- Environmental liability

- Emerging technology risks

The flexibility of the Lloyd’s market makes it particularly attractive for businesses operating in industries where standard insurance policies may not provide sufficient protection.

Who Uses Lloyd’s?

Most Lloyd’s clients are organizations rather than individual consumers.

Its marketplace serves a wide variety of industries, including:

- Banks

- Brokerage firms

- Fintech companies

- Investment managers

- Insurance companies

- Shipping operators

- Airlines

- Energy companies

- Construction firms

- Technology businesses

- Government organizations

Large multinational corporations frequently rely on Lloyd’s because their operations involve risks that require customized underwriting and significant insurance capacity.

Benefits of Lloyd’s

Lloyd’s has maintained its global reputation for more than three centuries for several reasons.

Its main advantages include:

- Access to highly specialized insurance expertise.

- Large underwriting capacity for complex risks.

- Flexible policy structures.

- Global recognition and reputation.

- Financial strength through risk distribution.

- Ability to insure emerging industries and new technologies.

The marketplace structure also encourages competition between syndicates, often resulting in tailored insurance solutions that better reflect each client’s unique risk profile.

Limitations to Consider

Although Lloyd’s is widely respected, it is not designed for every insurance need.

Some limitations include:

- Policies are generally arranged through brokers rather than directly with customers.

- Insurance terms vary depending on participating syndicates.

- Products are primarily designed for commercial clients.

- Coverage for highly specialized risks can be more expensive than standard insurance.

- The marketplace structure may appear more complex than dealing with a traditional insurer.

Businesses considering Lloyd’s should work with experienced brokers who understand how the marketplace operates and can negotiate appropriate coverage.

Final Verdict

Lloyd’s of London remains one of the world’s most important specialty insurance markets. Its unique marketplace model enables multiple independent insurers to work together, providing protection for risks that conventional insurance companies often cannot accommodate.

For businesses operating internationally or facing complex financial, technological, or operational risks, Lloyd’s offers a level of flexibility and underwriting expertise that few insurance markets can match.

While it is not intended for everyday consumer insurance, Lloyd’s continues to set the global standard for commercial and specialty risk insurance, making it a trusted choice for organizations seeking sophisticated insurance solutions.